Social Security in 2026: Projected Changes and Their Impact

Understanding the Looming Fiscal Challenges

The Social Security program faces well-documented fiscal challenges, primarily driven by demographic shifts and economic factors. The ratio of workers contributing to retirees receiving benefits is declining, placing increased strain on the system’s long-term solvency.

Experts and government agencies have consistently highlighted these pressures, indicating that without legislative action, the trust funds could face depletion in the coming years. This context is crucial for comprehending why adjustments to Social Security are not just possible, but increasingly probable.

The ongoing debate revolves around various proposals designed to shore up the program, ranging from benefit modifications to revenue enhancements. Each potential solution carries its own set of beneficiaries and detractors, making political consensus a complex endeavor.

Demographic Shifts and Trust Fund Solvency

The aging of the baby-boomer generation and lower birth rates mean fewer workers are supporting more retirees. This fundamental demographic imbalance is a primary driver of Social Security’s long-term financial outlook, influencing projections for 2026 and beyond.

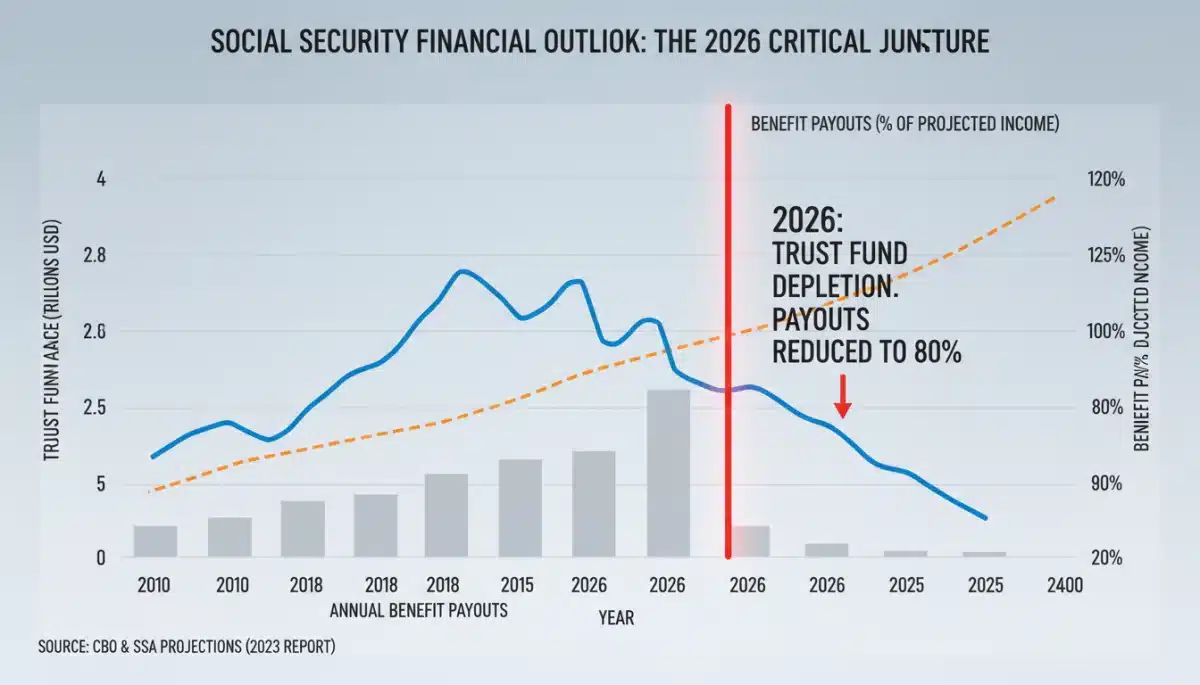

The annual reports from the Social Security Administration’s Board of Trustees consistently project that the Old-Age and Survivors Insurance (OASI) Trust Fund will be able to pay 100 percent of scheduled benefits until a certain point, after which it would only be able to pay a reduced percentage if no legislative changes occur.

These projections are critical for understanding the urgency behind potential reforms to Social Security.

- The worker-to-beneficiary ratio continues to decline, from 2.8 in 2000 to approximately 2.6 today, and is projected to fall further.

- The OASI Trust Fund is currently projected to be able to pay 100% of scheduled benefits until the mid-2030s.

- Without legislative action, benefit payments would then be reduced, underscoring the need for proactive measures.

Potential Policy Adjustments on the Horizon

Various policy proposals are currently under consideration to address the long-term solvency of Social Security. These proposals generally fall into two broad categories: those that increase revenue and those that adjust benefits, each with distinct implications for future retirees.

Some suggestions involve raising the full retirement age, altering the cost-of-living adjustments (COLAs), or modifying the formula used to calculate initial benefits. On the revenue side, discussions often center on increasing the Social Security tax rate or raising the maximum earnings subject to Social Security taxes.

The political landscape makes any definitive prediction challenging, but the need for action is widely acknowledged. Understanding these potential adjustments is key to preparing for the impact of Social Security.

Raising the Full Retirement Age

One frequently discussed policy adjustment is increasing the full retirement age (FRA), which is currently 67 for those born in 1960 or later.

Proponents argue this aligns with increased life expectancies and would reduce the total payout period for benefits.

Such a change would mean individuals would have to work longer to receive their full benefits or accept reduced benefits if they claim earlier.

This could significantly alter retirement planning strategies for those nearing retirement age, impacting the financial outlook of Social Security.

- Raising the FRA could lead to a reduction in lifetime benefits for many individuals.

- It would necessitate longer working careers for those seeking full benefits.

- The economic impact could disproportionately affect those in physically demanding jobs.

Adjusting Cost-of-Living Allowances (COLAs)

Another area of potential reform involves the Cost-of-Living Adjustments (COLAs), which are designed to help Social Security benefits keep pace with inflation. Modifying the COLA formula, such as by using a different inflation index, could result in smaller annual benefit increases.

While seemingly minor, even small reductions in COLAs can accumulate over a retiree’s lifetime, significantly impacting their purchasing power.

This adjustment is often considered because it can yield substantial savings for the program without directly cutting current benefits, yet it remains a contentious point in discussions about Social Security.

Impact on Future Retirees: What to Expect

For individuals planning to retire in 2026 or later, the projected changes to Social Security carry significant implications. These alterations could reshape retirement income streams, requiring adjustments to personal financial strategies and expectations.

Future retirees might need to consider working longer, increasing personal savings, or diversifying their retirement portfolios to compensate for potential shifts in Social Security benefits. The exact nature of the impact will, of course, depend on the specific legislative actions taken.

It is imperative for those nearing retirement to stay informed about these developments and consult with financial advisors to understand how potential changes to Social Security might affect their individual circumstances.

Navigating Reduced Benefit Scenarios

Should benefit reductions or slower growth in benefits materialize, future retirees will need robust strategies.

This might include re-evaluating retirement timelines, exploring part-time work options in retirement, or adjusting spending habits to align with potentially lower Social Security income.

Financial planners are already advising clients to not solely rely on Social Security for retirement income, emphasizing the importance of diverse savings and investment vehicles. Proactive planning can mitigate the adverse effects of any changes to Social Security.

- Diversify income sources beyond Social Security, including 401(k)s, IRAs, and personal savings.

- Consider delaying Social Security claims if feasible, to maximize monthly benefit amounts.

- Explore part-time work or side gigs to supplement retirement income.

Economic Repercussions and Broader Context

The modifications to Social Security are not isolated events; they operate within a broader economic context.

Any significant changes could have ripple effects across the economy, influencing consumer spending, housing markets, and the overall financial stability of older Americans.

Economists are closely monitoring how various proposals might impact different demographic groups, particularly those with lower incomes or limited alternative retirement savings. The goal is to ensure the program’s solvency while minimizing adverse effects on vulnerable populations.

The decisions made regarding Social Security will therefore reflect a delicate balance between fiscal responsibility and social equity, with far-reaching consequences for the nation’s economic health.

Impact on Consumer Spending and Savings

A reduction in future Social Security benefits could lead to a decrease in consumer spending among retirees, potentially slowing economic growth.

Conversely, increased awareness of impending changes might spur higher savings rates among younger generations, which could boost capital formation in the long run.

The interplay between individual financial decisions and national economic trends highlights the complexity of Social Security reform. Policymakers must weigh these broader economic impacts when considering adjustments to Social Security.

Legislative Outlook and Political Discourse

The path to Social Security reform is inherently political, involving intense debate and negotiation between various stakeholders. The bipartisan nature of the challenge means that any viable solution will likely require compromise from both sides of the political spectrum.

As 2026 draws closer, the urgency for legislative action will undoubtedly intensify. Lawmakers are under pressure to devise sustainable solutions that protect current beneficiaries while ensuring the program’s viability for future generations.

The discourse surrounding Social Security will remain a prominent feature of US politics, with every proposal scrutinized for its economic and social implications.

Key Players and Advocacy Groups

Numerous organizations and individuals play crucial roles in shaping the Social Security debate. Advocacy groups representing retirees, workers, and specific demographic segments actively lobby policymakers, presenting diverse perspectives on reform options.

These groups often highlight the potential impact of changes on their constituents, adding layers of complexity to legislative efforts.

Understanding the positions of these key players provides insight into the likely directions of reform for Social Security.

- AARP frequently advocates for protecting current and future retiree benefits.

- The Committee for a Responsible Federal Budget often emphasizes fiscal sustainability and long-term solvency.

- Various labor unions advocate for maintaining strong worker benefits and contributions.

Personal Preparedness: Strategies for Future Retirees

Given the uncertainty surrounding future Social Security benefits, personal preparedness becomes even more critical for those planning retirement. Proactive steps can significantly cushion the impact of any potential changes, ensuring a more secure financial future.

Developing a comprehensive retirement plan that accounts for various scenarios, including potentially reduced Social Security income, is a prudent approach. This involves a thorough assessment of current savings, investment strategies, and anticipated retirement expenses.

Engaging with financial professionals to craft a personalized strategy is highly recommended for anyone concerned about the implications of Social Security.

Diversifying Retirement Income Sources

Relying solely on Social Security for retirement income is increasingly risky. Diversifying income sources through personal savings, 401(k)s, IRAs, pensions, and other investments is essential. This multi-faceted approach provides greater financial resilience against unforeseen changes.

The goal is to create a robust financial safety net that can withstand adjustments to Social Security or other economic shifts. This strategy is particularly vital as discussions continue regarding Social Security.

- Maximize contributions to tax-advantaged retirement accounts like 401(k)s and IRAs.

- Explore investment opportunities that align with your risk tolerance and long-term goals.

- Consider annuities or other income-generating products to supplement traditional retirement savings.

Monitoring Official Announcements and Reports

Staying informed about the latest developments is crucial for anyone whose retirement plans could be affected. This involves regularly monitoring official announcements from the Social Security Administration, congressional committees, and reputable financial news outlets.

The Board of Trustees’ annual report provides the most authoritative projections and analyses of Social Security’s financial status. These reports offer valuable insights into the program’s health and the potential timing and nature of future adjustments.

Paying close attention to legislative proposals and public discourse will provide early indicators of how Social Security might evolve, allowing for timely adjustments to personal financial plans.

Where to Find Reliable Information

Official government websites, such as the Social Security Administration (SSA.gov), are primary sources for accurate and up-to-date information.

Additionally, non-partisan research organizations and established financial news agencies often provide insightful analyses based on verified data.

Avoid speculative or unverified sources, especially when making critical financial decisions. Rely on information directly attributable to official statements or expert consensus when assessing the future of Social Security.

| Key Point | Brief Description |

|---|---|

| Fiscal Challenges | Demographic shifts and economic factors strain Social Security’s long-term solvency. |

| Policy Adjustments | Proposals include raising retirement age, altering COLAs, or increasing payroll taxes. |

| Future Retiree Impact | Potential changes could reshape retirement income, requiring proactive financial planning. |

| Legislative Outlook | Bipartisan consensus and compromise are needed for sustainable reform solutions. |

Frequently Asked Questions About Social Security in 2026

The primary reasons stem from demographic shifts, specifically a declining worker-to-beneficiary ratio and increased life expectancies. These factors place significant strain on the Social Security trust funds, necessitating adjustments to ensure the program’s long-term solvency for future generations.

One common proposal involves gradually raising the full retirement age beyond the current 67. While no definitive changes are enacted, discussions suggest this could be a way to reduce total benefit payouts over time, impacting those planning to retire in or after 2026.

While no direct cuts to current benefits are expected, future benefits could be adjusted through changes like modified cost-of-living allowances or a higher full retirement age. The extent of any reduction depends on legislative action, which is still under debate for Social Security in 2026: Projected Changes and Their Impact on Future Retirees.

Future retirees should focus on diversifying their retirement income sources beyond Social Security, increasing personal savings, and consulting with financial advisors. Understanding potential policy adjustments and staying informed about legislative progress is also crucial for proactive planning.

The most reliable information comes directly from the Social Security Administration (SSA.gov), particularly their annual Board of Trustees’ reports. Reputable financial news outlets and non-partisan research organizations also provide accurate analyses and updates on the ongoing discussions and potential reforms.